Inaccurate financial reporting can wreak havoc on businesses. It leads to poor decisions and financial instability.

Accurate financial reporting is crucial for any business. When reports are inaccurate, it can cause confusion and mistrust. Investors, stakeholders, and management rely on precise financial data to make informed decisions. Inaccuracies can stem from various sources such as human error, fraud, or outdated software.

These mistakes can result in significant financial losses, legal troubles, and damaged reputations. It is vital to understand the common causes of inaccurate financial reporting and how to prevent them. This blog will explore these causes and offer solutions to ensure your financial reports are always reliable. Stay tuned to learn how to protect your business from the pitfalls of inaccurate financial reporting.

Common Causes

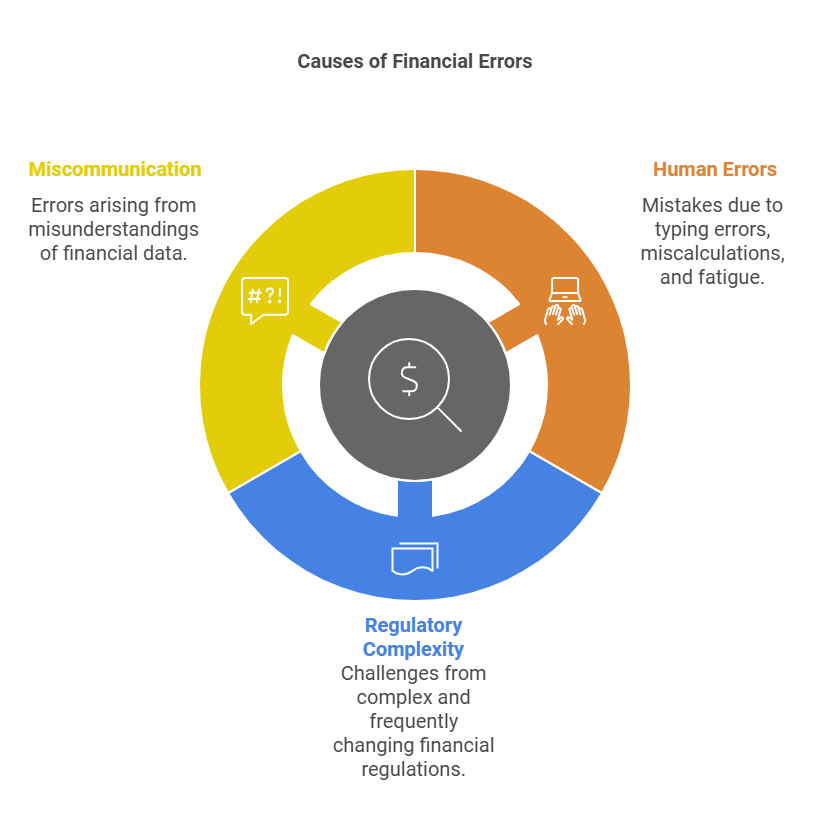

Human errors are a big cause of financial mistakes. People often make typing errors or miscalculate numbers. Fatigue and lack of training can also lead to mistakes. Even a small error can cause big problems in reports. Errors can also come from miscommunication or misunderstanding of financial data. Regular reviews and checks can help catch these errors.

Financial regulations are often very complex. Many rules are hard to understand. This can lead to mistakes in financial reports. Frequent changes in regulations add to the confusion. Companies need to stay updated with new rules to avoid errors. Hiring experts can help, but it is not always enough. Clear and simple guidelines can reduce mistakes.

Impact On Businesses

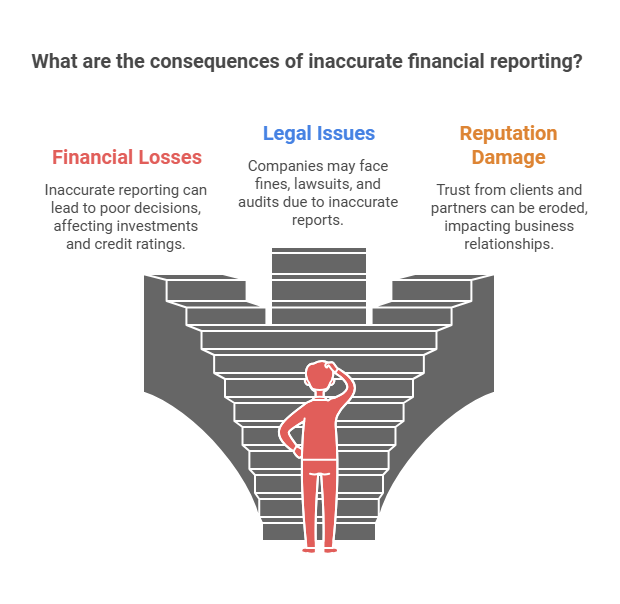

Inaccurate financial reporting can cause huge losses. Companies may lose money due to wrong decisions. Investors might pull out their funds, leading to a drop in stock prices. Misleading data can result in bad investments. The firm’s credit rating might suffer. This can make loans more expensive. Small mistakes can lead to big financial troubles.

Companies can face legal issues due to inaccurate financial reports. Regulatory bodies might impose fines. Lawsuits from shareholders can arise. Directors and officers might face personal liability. Legal fees can add up quickly. Incorrect reports can lead to audits. This creates extra costs and stress. The company’s reputation can also suffer greatly. Trust from clients and partners can be lost.

Role Of Technology

Technology can contribute to inaccurate financial reporting due to software errors or data entry mistakes. Automated systems can misinterpret complex financial transactions, leading to misleading information.

Automation Tools

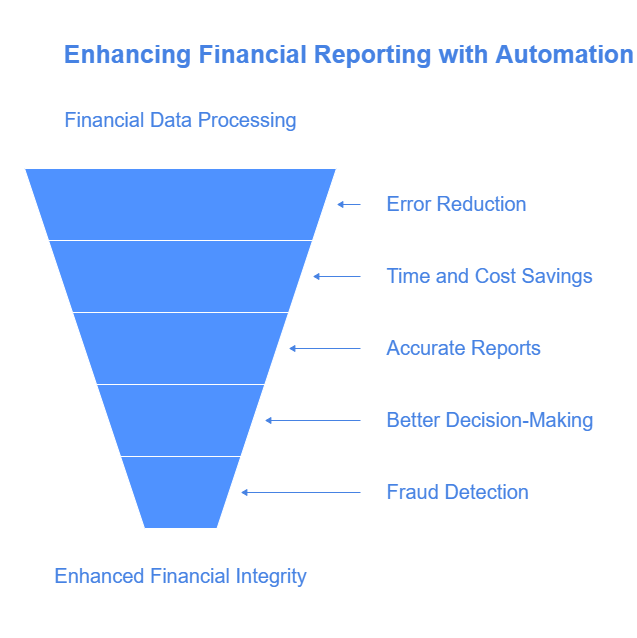

Automation tools help reduce errors in financial reporting. These tools perform tasks faster and with more accuracy. Humans make mistakes, but machines follow rules. Using automation tools, companies save time and money. Businesses also get more accurate financial reports. This helps in making better decisions. Automation tools also help in detecting fraud. They check each transaction carefully.

Data Analytics

Data analytics plays a key role in financial reporting. It helps in finding patterns and trends in data. By using data analytics, companies can predict future financial outcomes. This helps in planning better. Data analytics also helps in identifying errors. It checks large amounts of data quickly. This ensures more accurate financial reports. Companies can rely on these reports for critical decisions.

Training And Education

Effective training and education can reduce inaccurate financial reporting. Employees learn proper methods to ensure correct data entry. This minimizes errors and helps maintain financial accuracy.

Employee Workshops

Employee workshops are crucial for accurate financial reporting. These workshops help staff understand financial standards. Employees learn how to record data correctly. Errors in reports often come from a lack of training. A well-trained team reduces mistakes. Workshops should be held regularly. Consistent training keeps skills fresh. It ensures everyone is up-to-date with the latest practices.

Continuous Learning

Continuous learning is key in financial reporting. Financial rules change often. Staff must stay informed. Regular updates and training sessions help. It prevents outdated methods. Learning should be a part of daily tasks. Short, frequent lessons are effective. They fit into busy schedules. Continuous learning fosters a culture of accuracy.

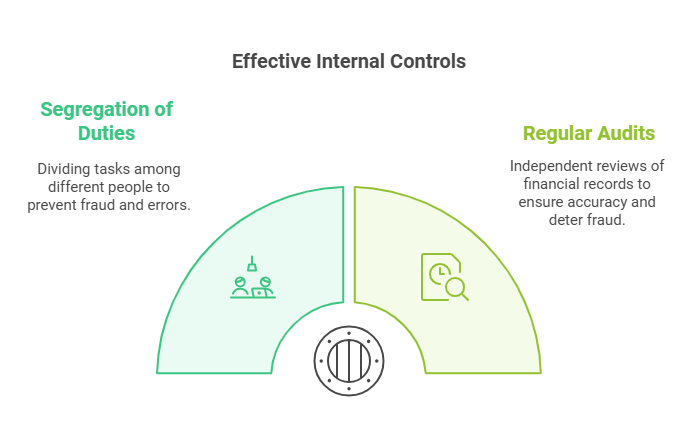

Effective Internal Controls

Segregation of duties means splitting tasks among different people. This prevents one person from having too much control. For example, one person records transactions. Another person reviews them. This way, errors and fraud are less likely to happen. It adds a layer of security to financial processes.

Regular audits check financial records for accuracy. They help find mistakes or fraud. Audits should be done by someone independent. This ensures a fresh look at the data. Regular checks keep everyone on their toes. They know their work will be reviewed. This encourages better practices.

Quality Assurance Processes

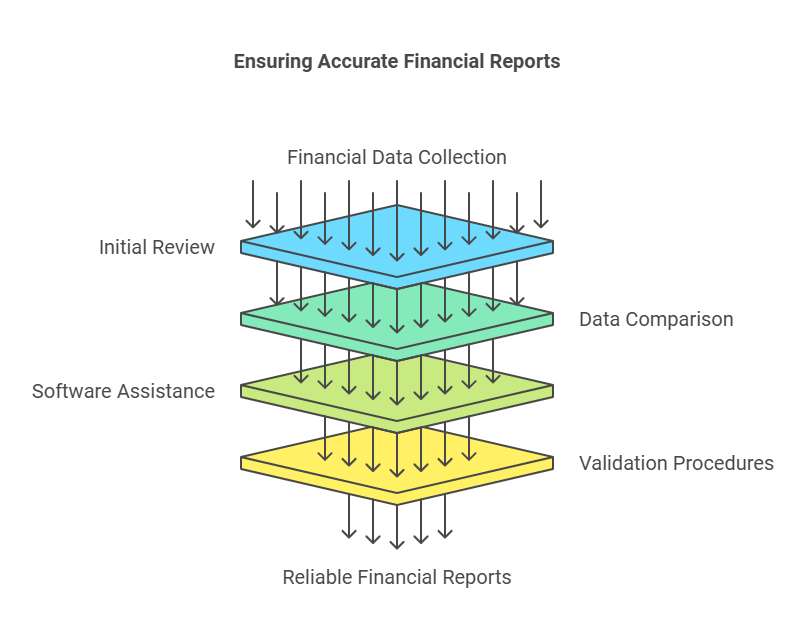

Review mechanisms help find mistakes in financial reports. Teams check figures twice. They compare numbers with past data. This helps spot any errors. Mistakes can lead to wrong conclusions. Correct numbers are very important. Teams often use software for this task. It makes the job easier. Software can check many numbers quickly. This saves time and effort.

Validation procedures are steps to ensure data is right. These steps are very important. They help confirm that data is correct. First, the team collects all data. They check if data is complete. Then, they check if data is accurate. They match data with source documents. This helps to prevent errors. Validation is a key part of quality assurance. Proper validation ensures reliable reports.

Regulatory Compliance

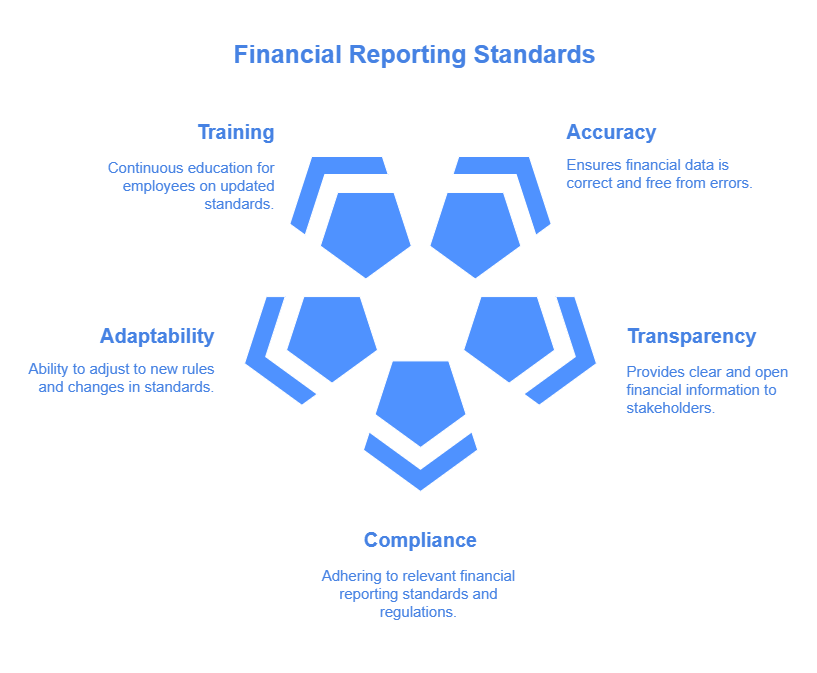

Financial reporting standards help keep records clear. Companies must follow these rules. These rules ensure accuracy and transparency. Different countries have different standards. International standards like IFRS are common. US companies follow GAAP rules. Understanding these standards is key. It helps avoid errors.

Rules change over time. It is important to stay updated. New laws can affect financial reports. Regular training helps. Employees need to learn new rules. Companies must monitor changes. Use tools and resources to stay informed. This helps avoid mistakes.

Case Studies

Companies have found ways to fix financial reporting problems. One company used new software to track all transactions. Another firm hired a financial expert to review their reports. Both companies saw improvements in their financial accuracy.

Accurate reporting is crucial for business health. First, always double-check numbers. Second, use trusted software for recording transactions. Third, hire qualified staff to handle finances. Lastly, regular audits can catch errors early. These steps help ensure accuracy and build trust with stakeholders.

Frequently Asked Questions

What Causes Inaccurate Financial Reporting?

Inaccurate financial reporting can result from human errors, fraud, inadequate internal controls, or outdated software. Ensuring proper training and implementing robust systems can help mitigate these risks.

How Can Businesses Avoid Financial Reporting Errors?

Businesses can avoid errors by conducting regular audits, maintaining accurate records, and implementing strong internal controls. Continuous staff training and using reliable accounting software are also crucial.

What Are The Consequences Of Inaccurate Financial Reporting?

Consequences include legal penalties, loss of investor trust, damaged reputation, and financial losses. Ensuring accurate reporting is vital for maintaining business integrity and compliance.

How Does Inaccurate Reporting Affect Stakeholders?

Inaccurate reporting misleads stakeholders, leading to poor decision-making. It can erode trust, impact investments, and damage the company’s reputation in the market.

Conclusion

Accurate financial reporting is crucial for business success. It builds trust and avoids legal troubles. Regular audits help catch errors early. Always double-check numbers before submitting reports. Training staff ensures they understand reporting standards. Good practices protect your company’s reputation.

Remember, clear and honest reporting benefits everyone involved. Your business can thrive with proper financial management. Stay vigilant and committed to accuracy. This approach will foster growth and stability.